Mobile banking is now central to how people manage their finances. Whether it’s checking balances, paying bills, or transferring funds, users expect fast and secure access to their accounts from anywhere.

According to Allied Market Research, the global mobile banking market was valued at $1.5 billion in 2022 and is projected to reach $7 billion by 2032, growing at a CAGR of 16.8% from 2023 to 2032. This growth reflects increasing user demand, but it also brings higher expectations around security.

Despite its popularity, many users remain cautious about mobile banking. Concerns around data privacy, unauthorized access, and cyber threats still prevent a significant portion of potential users from adopting these platforms. This trust gap is especially visible among older demographics.

To build user confidence, your mobile banking app must do more than deliver convenience. It needs strong, clearly visible security across every layer. When users feel their financial data is safe, they are more likely to use and rely on your platform.

Why are Banking Apps Vulnerable?

The architecture of mobile banking apps is usually prone to some serious mobile banking vulnerabilities that may lead to financial security breaches.

Basically, a mobile-based online banking app is a type of software that is directly connected to the bank’s backend system via Application Programming Interfaces (APIs).

Generally, these APIs are based on open source code, which is quite supportive of the app developers. However, sometimes these APIs may create vulnerable security loopholes for mobile banking applications.

Here, the irony is that web app firewalls or a source code protection may not reduce or solve these loopholes.

Online and mobile banking system attackers can take advantage of machine-to-machine interactions by creating shadow APIs on their own. Ironically, these shadow APIs do not resurface as compromised endpoints.

Here are some high-risk vulnerabilities that can dampen your mobile banking app’s performance:

Lack of a united app ownership

App ownership becomes one of the most dangerous vulnerabilities when it comes to securing mobile banking solutions. Usually, there are two owners in this case: one is the external owner, and another who works for the bank.

In the banking sector, the line of business managers has ownership of mobile banking apps. Another owner of the app is the IT department at the bank. Apart from this, there is an external entity that is involved in the mobile banking app development and the management of its APIs.

Such type of ownership creates serious security concerns as the above mentioned three owners are sharing the responsibility. Because of this, there is a strong possibility that something may go wrong at any time.

Insecure data storage

iOS and Android are official app stores that offer a unique level of security through a wide range of features, such as permission systems or TouchID. If you do not use them properly, you may face privacy based online threats, opening your crucial personal data to hackers.

Faulty communication

Mobile banking apps rely on continuous communication with external sources such as servers, authentication systems, and device-level technologies like Bluetooth and NFC in mobile apps. These integrations are essential for key features like contactless payments, two-factor authentication, and real-time data exchange.

However, if not implemented securely, this communication can become a weak point. Poor encryption, misconfigured APIs, or exposed tokens can lead to unauthorized access or data leakage.

Financial institutions, credit unions, and digital banking platforms must stay alert to these risks. Before we look at how to improve app security, let’s quickly examine some common vulnerabilities and fraud patterns seen across the industry.

Critical mobile banking fraud cases

Fake bank

Mobile banking security researchers are constantly detecting and preventing latest app based banking Trojans, Malware, fake banking apps, phishing attacks and brute force attacks that impact mobile banking apps.

FakeBank is one such spyware that monitors the verification messages that are sent by the bank to the customers. When mobile banking app users get a verification code, the spyware copies the same and sends it to hackers or cybercriminals.

Duplicate Flash Player

Duplicate Flash Player is a video application which is either installed via an infected SMS or predatory E-Mail that contains some malicious download link. Once the mobile device users install the app over a smartphone, it requests the mobile phone administrator rights via a permission prompt.

After this, the malware of the app creates a dummy login screen that gets visible when the user opens it next time. Once the user enters the user credentials or bank login credentials, the malware copies it and sends the data into the database of the malicious users that it can use later on.

Svpeng

Roman Unuchek, Kaspersky Lab’s senior malware analyst has found a new modification of mobile banking trojan Svpeng. It is one of the most dangerous mobile banking malware.

For example, the Trojan can draw itself over other apps and unofficial sources, give itself permissions to send and receive SMS, carry out financial transactions, make calls, and read contacts and grant itself device administrator rights and block any attempt to cancel this action.

What can financial institutions do for app security?

1. Add a multi-factor authentication feature

Simply requiring the submission of a single password before granting access to your customer’s bank account is a defense system which can be beaten.

By adding a multi-factor authentication or a two-factor authentication feature – such as generated one-time passwords or biometric authentication methods such as fingerprints – you add an additional layer of security which cannot easily be deceived.

2. Encourage the use of NFC-embedded SIM cards

While you can’t force this security option on your consumers, you can highly suggest it. An NFC-embedded SIM card is a SIM card that allows consumers to securely download their credit card information into the Near Field Communication (NFC) SIM card.

This mobile banking security tip is more of a means to protect the information of their financial accounts – by not carrying their actual card, and not swiping it, they lessen the risks that their credit card information could be compromised, potentially giving access to their mobile bank application.

3. End-to-end encryption

Many entities like payment cards, merchants, card brands, and issuing banks play a significant role in an online transactions. The exchange of loads of sensitive data worth billions of dollars takes place in a year. Due to this, it has become a hotspot for hackers.

End-to-End encryption is a solution to this massive threat as it ensures that data is safe and sound. It conducts security audits and penetration tests which takes the security measures to an extra mile.

4. Fingerprinting device

Introduction of Fingerprinting devices adds an extra layer in banking mobile apps. It obtains various sets of signals such as IP address, location, remote server, time of the day, device type, location, PIN code, public wi-fi details, screen seize, mobile-enabled internet browser, etc.

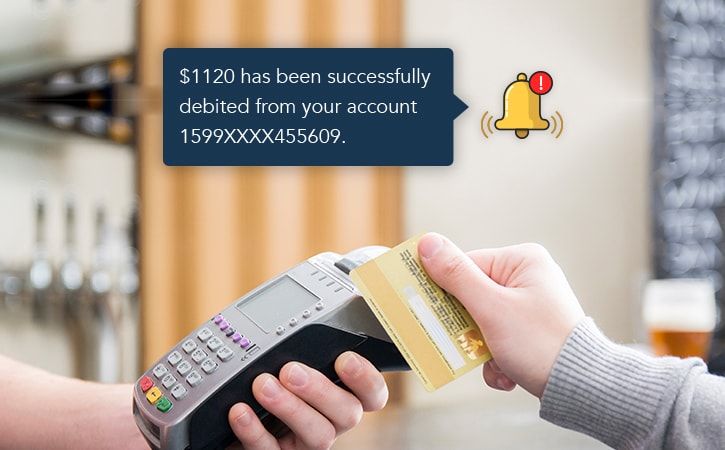

5. Offer real-time text and email alerts

It is safe to assume someone using mobile banking on their mobile browsers has direct access to their email and/or text messages.

By sending a quick, real-time email or text alert to notify a customer of account activity, they could easily prevent fraud, social engineering or an identity theft issue.

For example, some mobile bank applications allow you to be notified on your mobile devices if more than a customer-specified amount of money is spent.

This type of security feature could easily let someone know if the sensitive user information has been compromised, as they would likely be aware of such a large amount of money being spent from their account.

6. The power of paperless banking

The advent of IT technology and Mobile apps have had a massive impact on all sectors. Banking services and the financial sector are no exceptions; digitalization has transformed most of its processes.

With digitalization the banks can go completely paperless with most of its process, including something as basic as opening a bank account, account activation process, imparting accurate account activation instructions, money transfer confirmations and handling the online transaction.

Using digital or online platforms assist in increasing efficiency and transparency as all the file is in digital forms and their access becomes quick and convenient. To implement all these the banking institutions would require a mobile app solution provider which can provide them with an enterprise mobility solution.

7. Utilize behavior analysis

There is specialized software on the market that will monitor and analyze the banking login location, and online accounts activity of consumers.

Thanks to this technology, your mobile banking app could flag, several business logic errors, abnormal behavior or unauthorized access for further investigation.

Further investigation could be an email or text alert to the customer advising of suspicious activity, or a call from the bank further investigating the suspicious activity.

8. Safe digitalized documentation

Another way by which you can increase security of mobile banking app is through Safe Digitalized Documentation. Setting up an electronic signature can help in several verticals like eCommerce, call centers, retail branches, etc.

This method helps in bringing a huge portion of documentation on mobile which enables financial organizations to provide mobile banking customers with various benefits. And most importantly it avoids cases of fraud and thus increases the security.

9. Use secure access

By using a secure internet connection and positive technologies like HTTPS, customer account information can be better secured between the mobile web browser and the website they are connected to.

This technology will further protect customers against data theft and fraudulent logins.

Financial institutions often find themselves between a rock and a hard place – most customers want an acceptable level of convenience for mobile banking transactions.

But with mobile banking comes an increased security risk of critical vulnerabilities both for the bank and the mobile banking users.

Of course, the challenge is staying ahead of cyber criminals and continuously working to improve the security level of mobile banking applications and to make mobile banking safe.

By incorporating new technologies and agile development processes, financial institutions can continue to improve the risk score and security of their mobile apps and ward off the unwanted visitors – such as hackers.

Furthermore, these technologies will provide a strong authentication for mobile banking solution and wireless carriers of banking.

However, this is also a two-way street. In improving mobile bank application security, customers must also take their own precautions.

The financial institution that offer mobile banking applications should continue to educate customers and encourage them regarding Internet security and things that could put them at an increased risk of fraudulent activity.

PSD2 regulations

The chief aim of PSD2 regulations is to combat banking security flaws such as reverse engineering, theft of funds,. Along with this, PSD2 regulations also provide a strong defence mechanism against fraudulent activities and intends to increase digital security and enhance the usage of digital documents.

Moreover, it also supports the idea of open banking mobile technologies and improved online security.

PSD2 allows the financial companies, FinTech businesses, banks, big corporate firms and clients to work with banks via close co-ordination. Besides this, the law focuses on providing much improved online security to consumers in terms of online payments and customer experience overall.

Educate your customer

Your work doesn’t get finished by managing the financial security. You also have to make your customers aware of financial fraud too. In addition to this, clients should have to take precautions against financial fraud as well.

Apart from this, there are some critical authorization flaws or vulnerabilities in business logic can damage the mobile banking experience for the customers. Besides this, any banking transaction that took place via public wi-fi hotspots is also harmful.

This is why banks and financial institutions that are offering mobile applications need to educate mobile users about financial security. Banks need to guide customers on the latest mobile technologies to prevent frauds and steps to secure their finances.

Conclusion

Mobile apps have brought convenience and speed to modern banking, but they also come with increased exposure to cyber threats. Without proper security, sensitive user data and financial transactions remain vulnerable to attacks that can damage both trust and reputation.

The security practices outlined in this blog can help address the limitations of older systems and raise the safety standards of your mobile banking app. From secure authentication to encrypted communication and fraud prevention mechanisms, each measure plays a role in building a safer platform.

Your next step should be to consult with expert mobile application developers who understand the specific needs of financial platforms. Discuss the cost, scope, and feature set in detail to make sure your app is built with security at its core.